In this long-dated review, I focus on how the relationship between platinum imports and exports impact above-ground stocks and the platinum price. The industry does not report platinum import and export data either globally or by region. What then does the role of platinum imports and exports play in the supply-and-demand equation? Clearly, platinum imports and exports are closely related to supply and demand.

My calculations imply that global imports and exports amounted to c.14moz and c.7.3moz respectively in 2015. Note that global imports do not equal global exports as imports include a component of mine supply. My research shows that when adjustments are made to this component there is agreement between imports and exports. Global imports and exports showed a general upward trend between 1993 and 2008, which is consistent with an upward trend in platinum demand and price. Thereafter, imports and exports were in moderate decline. This general trend may be attributed in part to the global economic environment and a decline in the platinum price.

I am of the view that there are two main components that make up above-ground inventory, namely investment stock and working stock.My calculations imply that the working stock portion of the above-ground global inventory is large and refers to global exports. I estimate that the quantum of global working stock accounted for some 27% of global inventory (26.9moz) or c.7.3moz in 2015. By deduction, c.19.9moz of global inventory is likely to be held mainly by investors. Note that the China portion of global inventory, which amounts to c.8.1moz, is not mobile (China does not export platinum), leaving 11.8moz of investment stock potentially mobile. (My figures exclude exchange-traded funds, metal held by exchanges or working inventories of producers, refiners, fabricators or end-users).

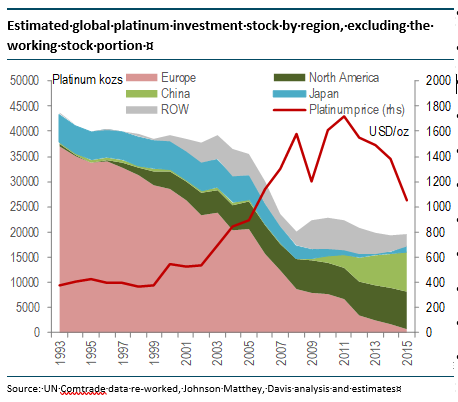

By excluding the working stock portion from each region, the investment stock trends are emphasised. Stocks in Europe and Japan declined considerably while stocks in North America, China and the Rest of the World increased. The most striking observation regarding regional trends in the investment stock portion of the above-ground inventory between 1993 and 2015 relates to the continued declining trend associated with Europe.

By excluding the investment stock from the global inventory, the working stock trends are emphasised and a relationship with the platinum price becomes apparent. In my view, the relationship between the working stock portion of the above-ground global inventory and platinum price is not surprising as working stock tends to increase with the price and vice versa.

My research shows that in 2015 (net of recycling and autocatalysts):

- Europe imported around c.5.0moz of platinum, which represented c.36% of global imports (around c.14.0moz).Europe exported c.4.3moz of platinum, which accounted for 58% of global exports (c.7.3moz) in 2015.

Platinum demand in Europe was c.1.8moz, which represents c.26% of estimated global demand (c.7.1moz – JM, DD) in 2015.

Clearly, the imbalance between imports, exports and demand implies a draw down in investment stocks. My calculations imply that in 2015 the rate of decline in above-ground inventory was c.1.1moz of which c.0.2moz is associated with the working stock portion and c.0.9moz is associated with the investment stock portion of the total inventory. Note my calculations imply that the above-ground inventory in Europe was estimated to be c.5.0moz in 2015.

It becomes obvious that the trends described above cannot continue indefinitely as the above-ground inventory will continue to diminish without a top-up by way of additional platinum imports from global investor holdings. Under these circumstances, I argue that upward pressure on the platinum price will be inevitable in the long term. Europe will likely have to look to the market for additional stocks in three to five years when stocks are likely to be depleted. In this regard, platinum prices are likely to remain weak over the next three to five years.Much, however, depends on the expected decline in South African mine production.

My research implies that Europe dominates global platinum imports and exports. In this regard, it appears that Europe acts as a global conduit for platinum, accounting for c.58% of global exports.

- North American imports and exports were c.1.4moz and c.0.7moz respectively in 2015.Both imports and exports have been in general decline since 2007. Exports accounted for c.10% of global exports (c.7.3moz).

Platinum demand in North America was c.0.6moz, which represents c.8% of estimated global demand (c.7.1moz – JM, DD) in 2015. These figures imply a relatively neutral balance between imports, exports and demand.

By the end of 2015, the above-ground inventory in North America was estimated at c. 8.1moz of which c.0.7moz, or c.9%, was attributed to the working stock portion while the investment stock portion was c.7.4moz, or c.91%, of the above-ground inventory.

My calculations imply that investment stocks are high (c.7.3moz). An increase in demand from Europe in order to bolster its stock levels together with a decline in South African mine supply might act as a trigger for North American investors to sell into the market at a price.

- China imported c.3.5moz in 2015, which represents c.25% of global imports (c.14.0moz). Imports into China have exceeded demand since 2009; therefore, there is evidence of increased activity in investment in platinum either by the Chinese government and/or in investment holdings.

Over the period between 2013 and 2015, China imported on average c.3.3moz, which is c.1.1moz above autocatalyst and jewellery demand. Should China continue this investment activity it will likely become an upside price risk in the long term. (Note that China does not export platinum.)

- Japan imported c.1.6moz of platinum, which represented c.11% of global imports (c.14.0moz). Imports have been in decline since 2008 although there is evidence that they started to increase year-on-year after 2014. Exports amounted to c.0.6moz, which accounted for c.9% of global exports (c.7.3moz) in 2015.

Platinum demand in Japan was c.1.3moz, which represented c.19% of estimated global demand (c.7.1moz – JM, DD) in 2015. These figures imply a marginally negative balance between imports, exports and demand, which means that a small draw down in stock occurred in 2015.

Iestimate that the above-ground inventory in Japan was c.1.6moz by the end of 2015. The working stock portion of the above-ground inventory was c.0.6moz, or c.38%, while the investment stock portion was c.1.0moz, or c.62%, of the above-ground inventory.

- The ROW imported c.2.6moz of platinum, which represented c.18% of global imports (c.14.0moz). ROW exported c.1.6moz, which accounted for c22% of global exports (c.7.3moz) in 2015.

My research implies that the above-ground inventory in the ROW was probably c.4.1moz by the end of 2015. The working stock portion accounted for c.1.6moz, or c.39%, while the investment stock portion was c. 2.5moz, or c.61%, of the estimated above-ground inventory.

In this short review, I have quantified the relationship between platinum above-ground stocks, and platinum imports and exports, globally and by region between 1993 and 2015.

Research shows that Europe dominates global platinum imports and exports. In this regard it appears that Europe acts as a global conduit for platinum, accounting for c.58% of global exports. Europe, however, has been consistently drawing on its investment stocks to maintain its current export demand. I argue that upward pressure on the platinum price will be inevitable in the long term without a top-up by way of additional platinum imports from global investor holdings. Platinum prices are likely to remain weak over the next three to five years although depends on demand and the rate of decline in South African mine supply.

About Dr David Davis PhD MSc MBL CEng CChem FIMMM FSAIMM FRIC

David has been associated with the South African mining industry and mining investment industry for the past 40 years. At present, David is working as an independent precious metal consultant. David’s PhD involved: “Studies in the catalytic reduction and decomposition of nitric oxide 1976”.